Harley Davidson insurance is more than just a legal requirement; it’s a vital shield for one of the most iconic motorcycle brands in the world. Whether you’re a proud owner of a Road Glide, a Softail Standard, or a Street 750, understanding your insurance options ensures peace of mind on every ride.

Why Harley Davidson Insurance Matters

Harley Davidson motorcycles are not just machines; they represent freedom, individuality, and lifestyle. But with prestige comes responsibility. High-value bikes like these are attractive targets for theft and often cost more to repair. That’s why a standard policy might not offer the protection you truly need.

Types of Coverage Available for Harley Davidson Motorcycles

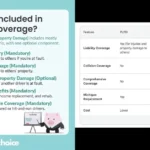

Liability Insurance

This is the minimum coverage required by law in most states. It covers damage you cause to other vehicles or property and medical expenses for other parties if you’re at fault in an accident. However, liability insurance does not cover your own bike’s damage.

Collision Coverage

This helps pay for repairs to your Harley if you collide with another vehicle or object, regardless of fault. For a high-end motorcycle, this coverage can save you from significant out-of-pocket costs.

Comprehensive Coverage

Comprehensive insurance handles non-collision-related damages such as theft, vandalism, fire, or weather events. Given the popularity and value of Harley Davidson bikes, this type of coverage is strongly recommended.

Uninsured/Underinsured Motorist Coverage

If you’re hit by a driver with little or no insurance, this coverage ensures that your medical and repair expenses are still taken care of.

Custom Parts and Equipment Coverage

Harley owners often customize their bikes. This optional coverage extends protection to aftermarket parts, custom paint jobs, and accessories, making it essential for fully covered enthusiasts.

Factors Influencing Harley Davidson Insurance Rates

Bike Model and Year

Some models, especially newer or limited-edition ones, command higher premiums due to their replacement cost.

Rider’s Age and Experience

Experienced riders with clean driving records generally pay less. Younger riders, particularly those under 25, face higher premiums.

Location

Urban areas with high traffic and theft rates tend to increase insurance costs. Conversely, rural riders might benefit from lower rates.

Usage

How often you ride and whether it’s for daily commuting or occasional joyrides affect the premium. More time on the road equals more exposure to risk.

Safety Features

Anti-theft systems, ABS, and GPS tracking can reduce your insurance rates.

Deductibles

Higher deductibles typically lower your premium but increase your out-of-pocket expense in the event of a claim.

Exclusive Harley Davidson Insurance Programs

Some insurers offer programs specifically tailored for Harley Davidson riders. These often include:

- Accident Forgiveness: Your first accident won’t raise your rates.

- OEM Parts Guarantee: Assurance that only genuine Harley parts are used in repairs.

- Disappearing Deductible: Your deductible drops over time if you remain claim-free.

- Trip Interruption Coverage: Helps with lodging and transportation if you break down far from home.

Comparison Table: Key Features of Harley Davidson Insurance

| Feature | Cost | Efficiency | Ease of Use | Scalability | Benefits |

| Liability Only | Low | Basic | Easy | Limited | Meets legal minimum |

| Collision + Liability | Medium | Moderate | Moderate | Moderate | Covers accidents |

| Full Coverage | High | High | Simple | Comprehensive | Maximum protection |

| OEM Parts Coverage | Slightly High | High | Seamless | Moderate | Genuine Harley parts |

| Custom Parts Inclusion | High | Excellent | Slightly Complex | Scales with add-ons | Protects customizations |

Real-World Scenarios: When Insurance Saves the Day

Imagine riding your Harley Davidson down a scenic route when a deer suddenly jumps in front of you. The collision causes substantial damage to your bike and injuries to your passenger. Without comprehensive and medical coverage, the out-of-pocket costs could be devastating.

Or picture coming out of a restaurant only to discover your Harley has vanished. With theft coverage, you won’t be financially stranded or forced to settle for a lesser replacement.

Emotional and Logical Reasons to Insure Your Harley

Motorcycles symbolize freedom, but accidents and theft can shatter that liberty in an instant. Emotionally, the thought of losing a prized Harley without coverage is heartbreaking. Logically, insurance helps avoid massive financial setbacks, legal troubles, and stressful disputes.

Common Mistakes Harley Owners Make

Skipping Comprehensive Coverage

Many assume their bike is safe in a garage. But fires, floods, and theft don’t knock before entering.

Undervaluing Custom Parts

Failing to disclose upgrades can leave you underinsured. Always declare custom work.

Choosing the Cheapest Policy

Low cost doesn’t always mean best value. Make sure you understand what your policy actually covers.

Ignoring Policy Updates

As your Harley ages or your riding habits change, your policy should evolve too. Annual reviews help optimize protection and cost.

Tips for Reducing Harley Davidson Insurance Premiums

- Take a motorcycle safety course.

- Bundle motorcycle insurance with auto or home policies.

- Increase your deductible to lower monthly premiums.

- Install security features like locks, alarms, and GPS trackers.

- Store your bike in a secure location.

How Claims Work for Harley Davidson Insurance

Filing a claim typically involves:

- Reporting the incident to your insurer immediately.

- Documenting the damage with photos and repair estimates.

- Providing witness statements if available.

- Cooperating with inspections or adjuster visits.

Most insurance companies aim to settle claims within 30 days, though timelines vary based on case complexity.

Choosing the Right Harley Davidson Insurance Provider

When selecting an insurer:

- Evaluate their reputation for motorcycle coverage.

- Look for specialized Harley programs.

- Compare multiple quotes.

- Check customer service ratings.

- Read policy fine print, especially on exclusions and limits.

Conclusion

Harley Davidson insurance is not a luxury; it’s a necessity for every rider who values their machine and personal safety. Whether you’re riding cross-country or commuting to work, the right coverage gives you the confidence to embrace the open road without hesitation.

FAQs

What is the average cost of Harley Davidson insurance?

Costs vary based on model, rider profile, and location, but typically range from $300 to $1,200 annually.

Can I get insurance for a vintage Harley Davidson?

Yes, many insurers offer classic motorcycle policies with agreed value and restoration coverage.

Does Harley Davidson insurance cover custom parts?

Only if you add custom parts coverage to your policy. It protects upgrades like saddlebags, exhausts, and custom paint.

Is full coverage worth it for an older Harley?

It depends on the bike’s value and your risk tolerance. If your Harley holds sentimental or collectible value, full coverage can be wise.

How can I lower my Harley Davidson insurance premium?

Take a safety course, bundle policies, increase your deductible, and add anti-theft devices to reduce rates.

What should I do if my Harley is stolen?

Report it to the police and your insurer immediately. Provide documentation like your title and recent photos to support your claim.